| “How’s the market?” is a question I am asked all the time. Now more than ever, the answer to this question is critical and detailed. You see, our market is experiencing a shift, a slowing down of price growth, if you will. Believe it or not, this is providing great opportunities for both buyers and sellers.

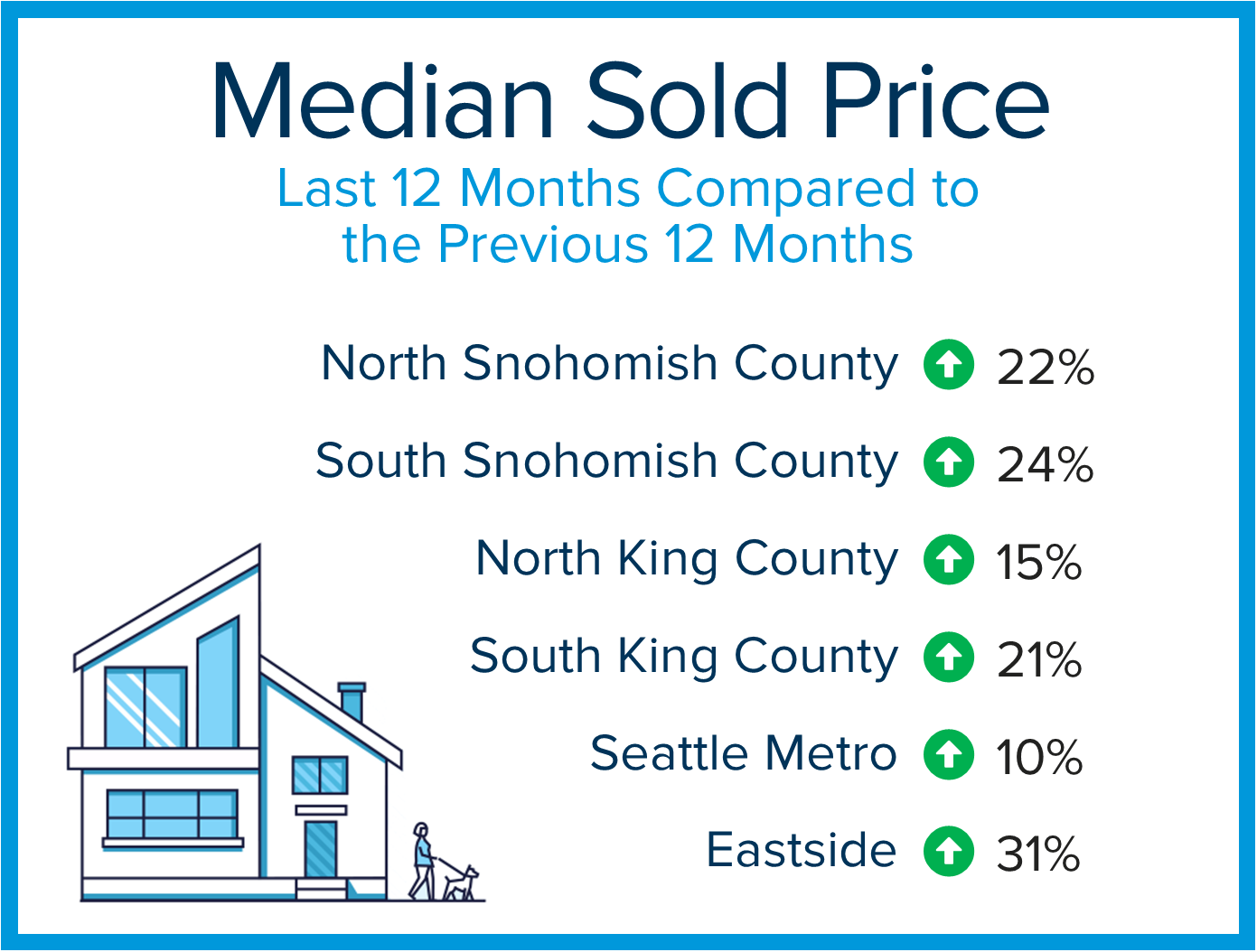

Let’s talk about the slow down in price appreciation first. What this means is when we get to the end of the year and average the last 12 months of median price and compare it to the previous 12 months of median price, we will still have a positive growth percentage, but that percentage will be lower than it was earlier in the year. You see, we had a very significant bump in prices in Q1 of 2022 that will level off as we complete 2022. Bear in mind that average home price appreciation rate long term is closer to 3-6% when comparing to the growth we’ve had recently.

Let me break this concept down for you with some numbers. In Snohomish County, in April of 2020, the median price was $520,000 and in April of 2022 the median price was $830,000 – this is a 60% increase in 2 years! In King County, in April of 2020, the median price was $720,000 and in April of 2022 the median price was $995,000 – this is a 38% increase in 2 years! That pace is unprecedented and unsustainable.

Let’s dig a little deeper! In Snohomish County, in December 2021 (the end of last year) the median price was $700,000 which was an above-average 35% increase from April 2020 (20 months). That means there was a 35% gain from April 2020 to December 2021 (20 months: $520,000 to $700,000 = 35%) but then a whopping 19% gain in 4 months, from December 2021 to April 2022 (4 months: $700,000 to $830,000 = 19%). This 4-month stretch of price growth is the root of the unsustainability and one that we will be leveling off of during this shift. It is very unlikely that we will return to prices below the December 2021 level, which was at an above-average growth rate of 35% from April 2020. The (unofficial) median price in May sits at $810,000 indicating the shift to settle somewhere between the April peak and where we landed at the end of last year. We must remember that we were celebrating price growth at the end of 2021!

In King County the numbers are not as extreme, but still well above average growth rates. In August 2021, the median price was $875,000 which was an above-average 22% increase from April 2020 (15 months). That means there was a 22% gain from April 2020 to August 2021 (15 months: $720,000 to $875,000 = 22%) and then a 14% gain in 9 months, from August 2021 to April 2022 (9 months: $875,000 to $995,000 = 14%). This 9-month stretch of price growth is one that will be leveling off during this shift. It is very unlikely we will return to prices below the August 2021 level, which was still an above-average growth rate of 22% from April 2020.

This is where perspective comes in and where pricing can get a little tricky. Coaching potential sellers as to why it would be unrealistic to expect the peak prices of Q1 2022 requires explaining the market factors that have played into this shift. The combination of the lowest inventory levels and lowest interest rates in history that took place in Q1 2022 was the perfect storm that created intense price growth over a short period of time. Now we must navigate the new environment as we chart our real estate goals. Three main factors have led to this much-needed tempering in price growth: inventory, interest rates/inflation, and affordability.

Inventory has finally started to grow although it is still a seller’s market. In Snohomish County, 2021 was an extreme seller’s market that never crested over 0.6 months of inventory; that’s just over two weeks! A seller’s market is defined as 0-3 months of inventory, a balanced market as 3-6 months, and a buyer’s market as 6-months plus. In May 2022, we sit at 0.9 months of inventory (unofficially). We have started to see more homes come to market, providing buyers with more selection. For example, in April 2020 there were 996 new listings; in December 2021 there were 525 new listings; in April 2022 there were 1,503 new listings (almost 3x as much over December), and (unofficially) in May there were 1,654 new listings. This additional selection is providing buyers the long-awaited option to find housing and has started to reduce the number of multiple offers which have put downward pressure on prices. When there is more selection, prices do not escalate as quickly.

In King County, for May 2022, we sit at 0.9 months of inventory (unofficially). In April 2020 there were 2,138 new listings; in December 2021 there were 1,103 new listings; in April 2022 there were 3,353 new listings (just over 3x as much over December), and (unofficially) in May 2022 there were 3,698 new listings.

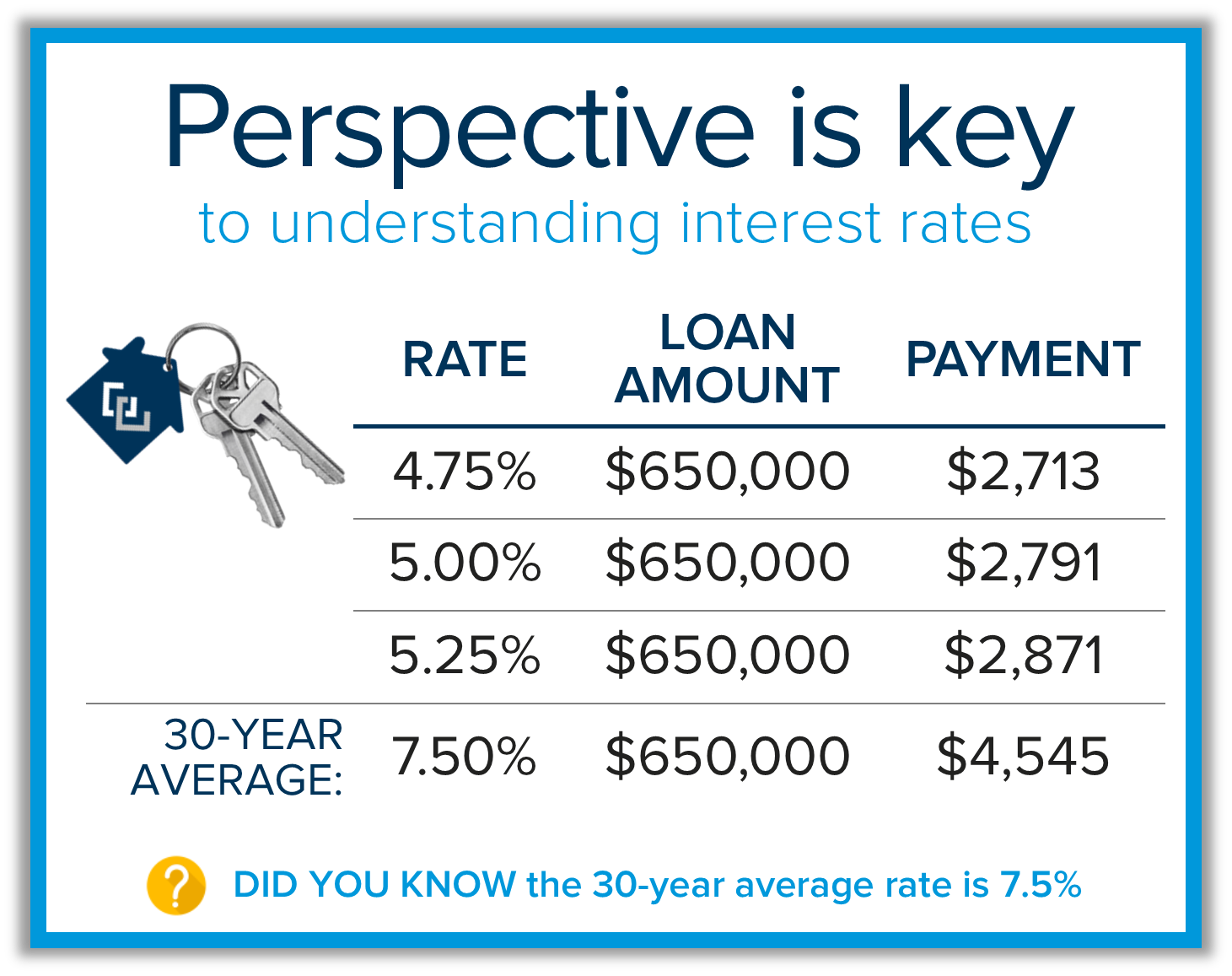

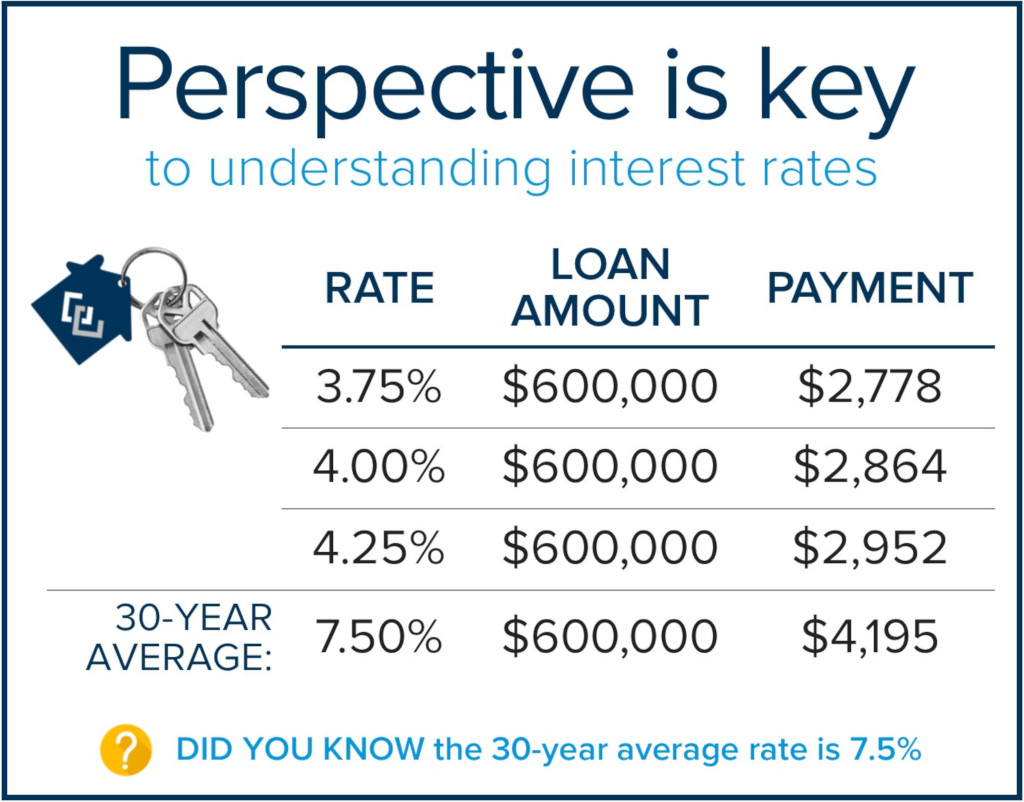

Interest rates have also grown over the last two years and even more specifically since the first of the year. We are currently hovering around 5%. At the start of 2022 we were hovering around 3%. The Fed finally gave way to the promise that rates would rise, which was a necessary tool to combat inflation. While 3%-4% rates were a dream, they were not a long-term reality. The 30-year average for interest rates is 7% which highlights that 5% is a great rate!

It is understandable that 5% pales in comparison to the historic lows we had, but those are most likely only going to be found in the history books in the foreseeable future. Rates being as low as 3% in Q1 2022 played into the rapid acceleration in price because it made the buyer audience larger when we had the least amount of inventory available. The good news is that while they had a quick 2-point increase from March 2022 to May 2022, they have seemed to stabilize. They have even come down a bit, making this our new normal for now, as future increases into 2023 are predicted. The good news for buyers who secured a home in Q1 is they also secured the lowest debt service in history, so they should be very happy.

Affordability has been a challenge for many, especially first-time home buyers. Affordability challenges at December 2021 prices were real, but the rise to April 2022 levels just plain removed buyers from the market. As price appreciation slows and prices level off due to the shift in market conditions, some buyers will be able to reenter the market and start to secure their wealth-building asset that also augments their lifestyle.

So, what does all of this mean? The word that keeps coming to my mind is perspective. We have walked through one of the most extreme seller’s markets of our time, which resulted in rapid price growth for sellers and limited choices for buyers. That is starting to ease up and we need to celebrate this! We are heading towards historical norms and while that is happening, we will need to keep the crazy Q1 price growth in a box alongside the unicorns and rainbows for the lucky sellers that found the pot of gold and buyers who secured the lowest rates ever. Good for them, but still good for anyone who has owned their home for longer than two years, as the amount of seller equity is abundant.

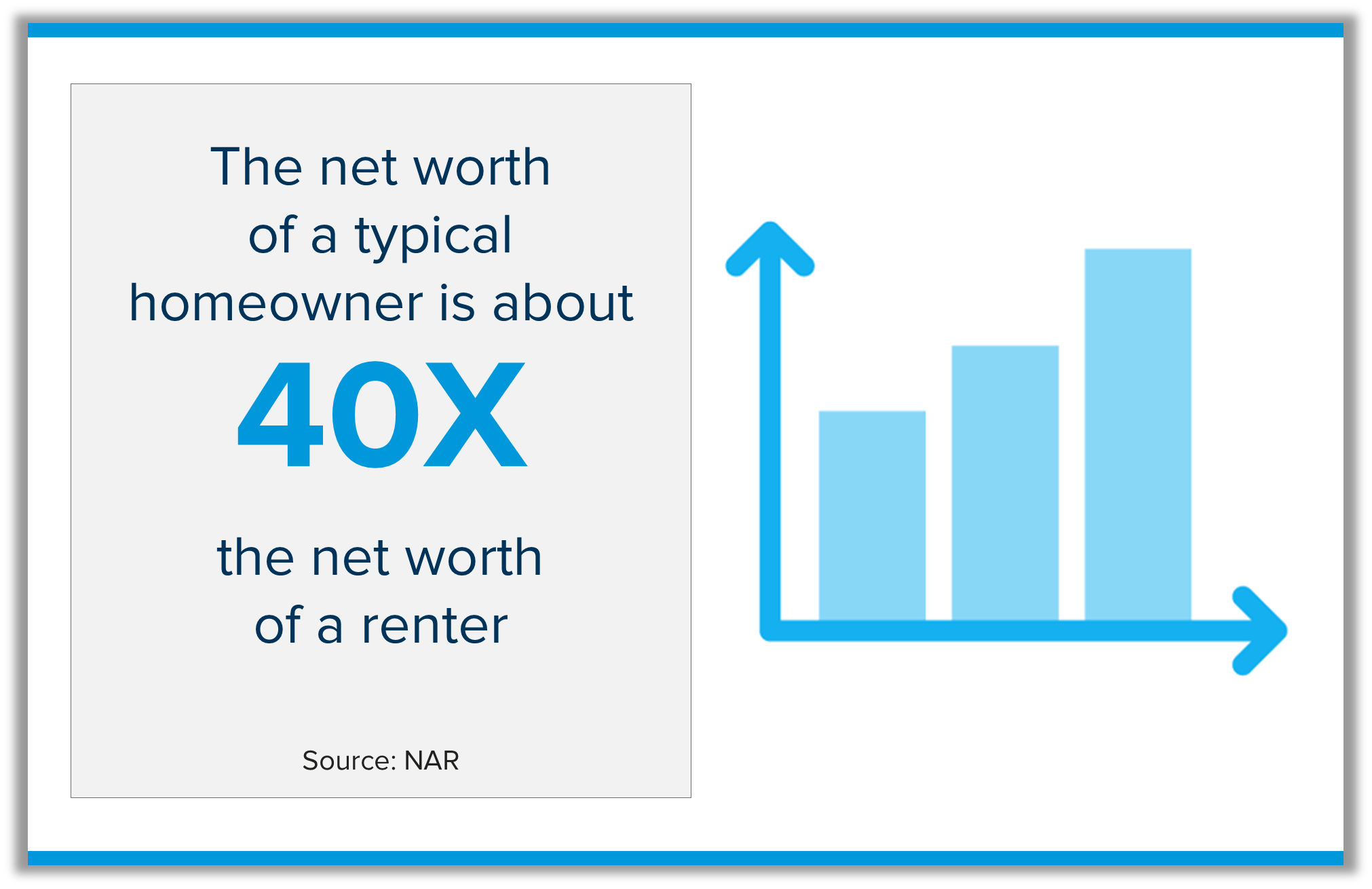

Real estate has always been a long-hold investment and we have lost sight of that with the abnormality of the last two years. Most importantly, real estate is a lifestyle decision. Our homes provide us shelter, community, features, and benefits. We make memories, find comfort, and if we are lucky, we are able to match our home to our lifestyle needs and build wealth at the same time.

With more selection, still-low interest rates, and coming off the crazy prices of Q1, more buyers will be able to make these lifestyle pivots more comfortably, all while sellers will still make phenomenal returns. Perspective is key to help see the forest through the trees, and if not taken into consideration could stall one from reaching their goals.

If you are curious about the value of your home in today’s market or are considering a purchase, please reach out. Even if you just want to talk these changes through and understand how they might affect your long-term goals. It is always my goal to help keep my clients well informed and empower strong decisions.

|

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If you attended our Virtual Economic Forecast Event last week with Matthew Gardner, did you see the mountain of socks?! Matthew is a bit of a sock aficionado, and we usually give him a gift of some fun or funny socks at our yearly event. This year, we decided to collect socks and donate them in Matthew’s name to

If you attended our Virtual Economic Forecast Event last week with Matthew Gardner, did you see the mountain of socks?! Matthew is a bit of a sock aficionado, and we usually give him a gift of some fun or funny socks at our yearly event. This year, we decided to collect socks and donate them in Matthew’s name to

The Windermere Ready Loan allows our home sellers to receive access to funds to make home improvements and merchandise their homes for the market with no upfront cost. Clients can borrow up to $50,000 as long as the Windermere Ready Loan and any other encumbrances on the property do not exceed 75% of the market value. With the majority of Puget Sound cities having experienced 15-25% in price appreciation over the last year or two, this loan-to-value ratio is very manageable.

The Windermere Ready Loan allows our home sellers to receive access to funds to make home improvements and merchandise their homes for the market with no upfront cost. Clients can borrow up to $50,000 as long as the Windermere Ready Loan and any other encumbrances on the property do not exceed 75% of the market value. With the majority of Puget Sound cities having experienced 15-25% in price appreciation over the last year or two, this loan-to-value ratio is very manageable.